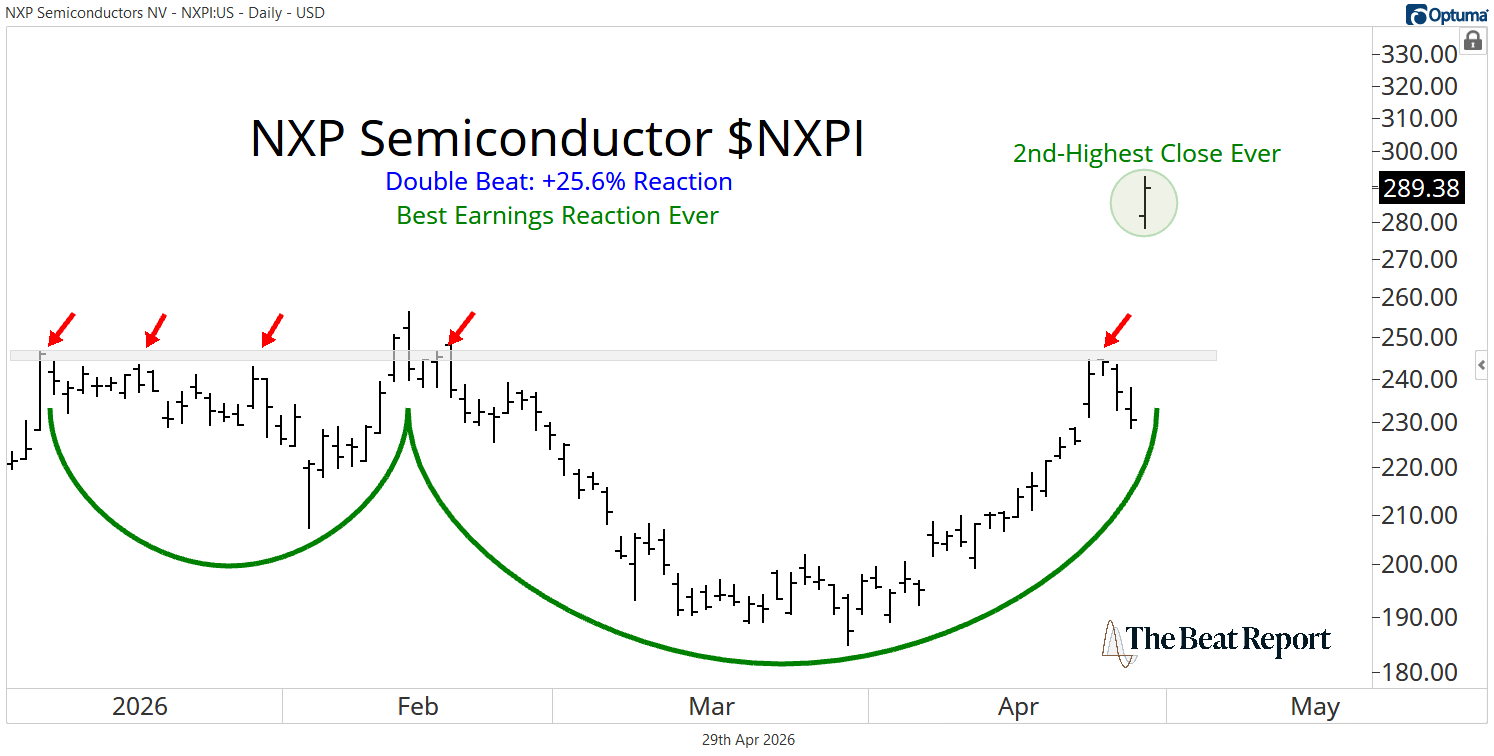

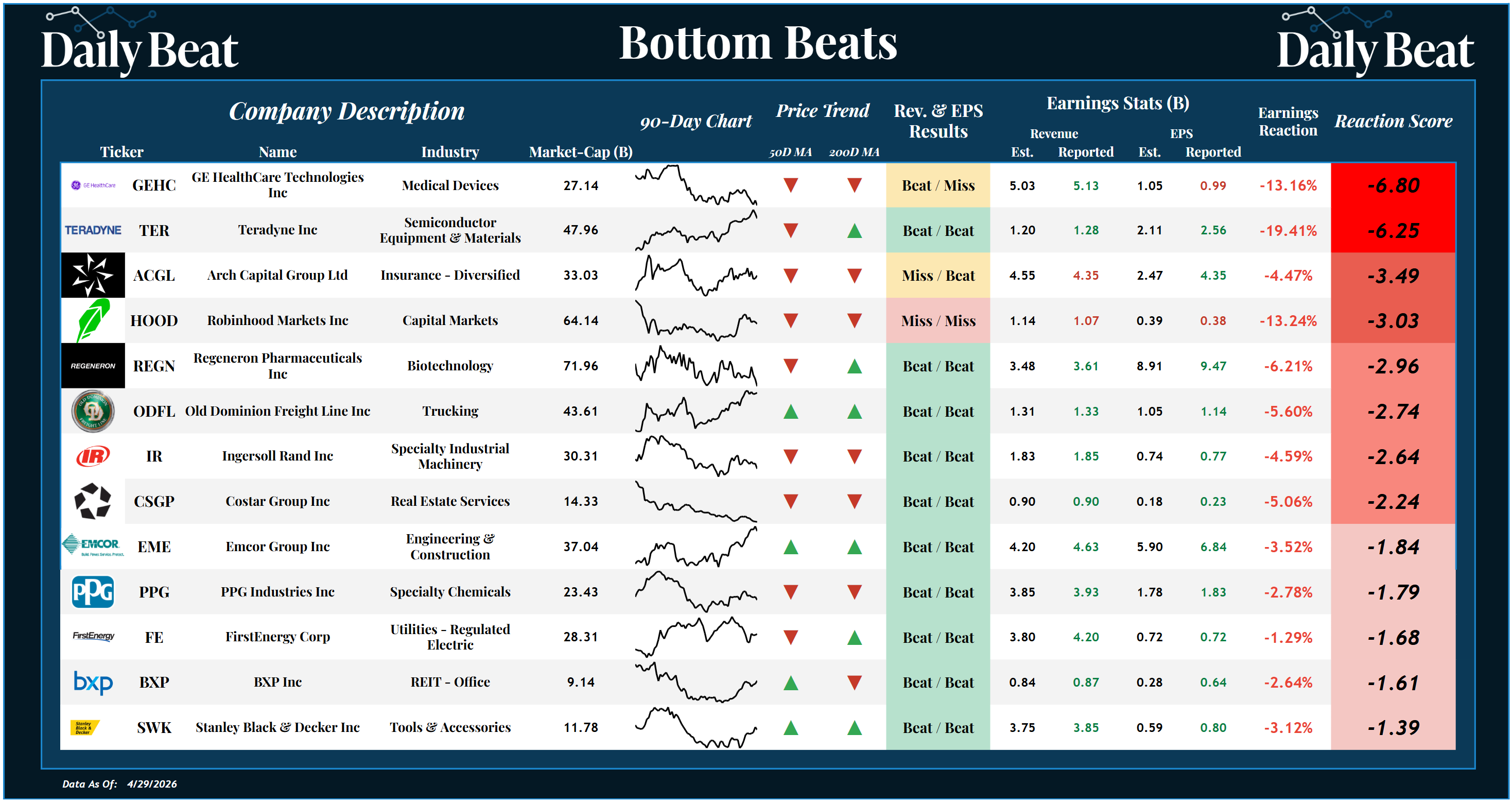

GE HealthCare has been carving out a massive distribution pattern over the past year, and now it's on the cusp of breaking down.

In the very short term, could this level hold and produce a bounce? Sure.

The stock is extremely oversold after a move like that, and it wouldn’t be surprising to see some kind of relief rally.

But stepping back and looking at the bigger picture, the trend is clearly lower, and the sellers remain in control.

And when you look under the hood, the fundamentals help explain why.

Yes, the company delivered solid top-line growth, with revenue coming in at the high end of expectations and strength across key segments like imaging and pharmaceutical diagnostics.

Demand remains healthy globally, with strong order trends and backlog supporting future growth.

But the problem isn’t the revenue... It’s profitability.

Margins came under pressure due to rising input costs, including a roughly $100 million increase in memory chip pricing and another $100 million tied to oil and freight costs. This forced the management team to lower its full-year profit and free cash flow guidance.

That’s the kind of shift the market does not take lightly, especially for a stock that was already struggling.

So while the business still has solid demand and long-term innovation potential, the near-term headwinds are very real, and the market is repricing the stock accordingly.

If GEHC breaks below last year's low, we expect it to fall another 10% and retest its all-time low at $53.

At the Premium Beat Report, we’re tracking these reactions in real time using our proprietary reaction score to identify the stocks where technicals and fundamentals are aligned.

These are the trends we’re actively trading, and they’re the ones that can generate 3x, 5x, even 10x returns over time.

We hope you're enjoying this earnings season as much as we are,

-The Beat Team